The Pattern Is Not the Point

Capital is rarely destroyed by a bad forecast. It is destroyed by an assumption nobody went back to check.

Bryan J. Kaus

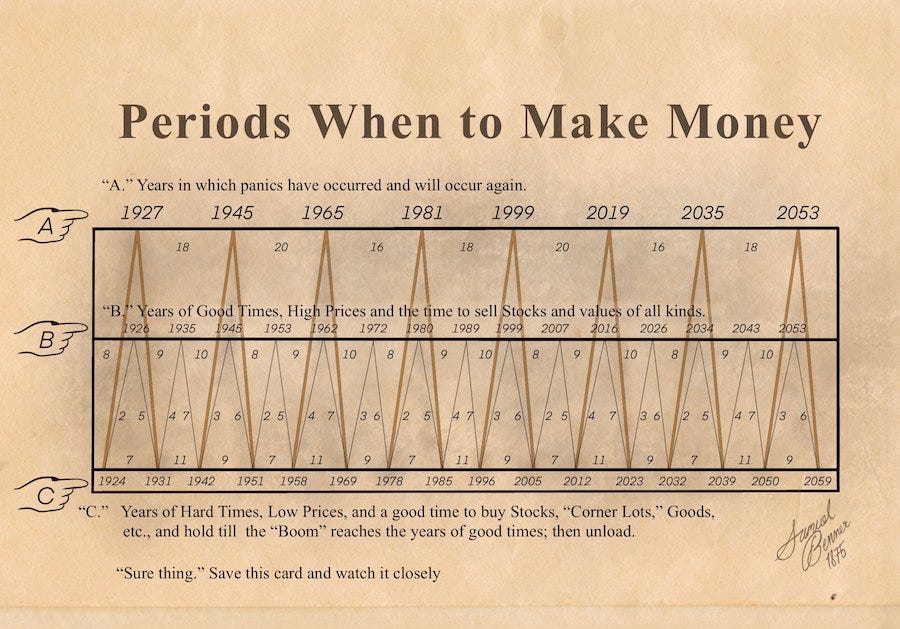

Sure thing. Save this card and watch it closely. Samuel Benner, 1875

There is a chart that keeps coming back.

Sepia paper, hand lettering, sawtooth peaks marching from 1924 out to 2059. Three rows, labeled panic, good times, hard times. It resurfaces every few years with a line attached, and the line is always some version of the same claim: an Ohio farmer in 1875 predicted 2008.

The dates land close enough to matter. 1927, near the crash of 1929. 1999, just ahead of the technology collapse. 2007, just ahead of the mortgage crisis. Off by a year or two, and the concession does real work, because a near miss reads as humility and humility reads as credibility.

It is a compelling object. It is also the most expensive idea in finance, wearing a costume.

The chart itself is harmless. Almost nobody is allocating against it. What is not harmless is the appetite that keeps pulling it back to the surface, because that appetite does not stay in the antique aisle. It shows up in trading accounts. It shows up in board packets and price decks. It showed up in the risk models of the largest financial institutions in the world, and it cost roughly a decade of growth. And it is now being wired, quietly and at scale, into the systems we are asking to think on our behalf.

Nobody sets out to destroy capital. That is the thing worth sitting with. Capital gets destroyed sideways, by people who were being careful, using good tools, right up until the moment the tool stopped describing the world and started replacing the judgment that was supposed to check it.

The chart is just the cleanest specimen of the impulse. So start there, then follow it into places where the money is real.

Start with the artifact, because the artifact is already lying

Before we evaluate the prophecy, look at the paper.

The card circulating as Benner’s 1875 forecast is not straightforwardly Benner’s. The “Periods When to Make Money” broadside is a business card of the George Tritch Hardware Company of Denver, compiled in 1872 and carrying copyright dates from the 1880s and 1890s. Benner published Benner’s Prophecies of Future Ups and Downs in Prices in 1875, a study of hog, corn and pig iron prices, and his original forecast ran out somewhere around 1891. The version now in circulation, the one that reaches 2059, is a later extension. Attribution between the two men is genuinely contested, and the chart most people are passing around is not the chart most people think they are passing around.

This is not a footnote. It is the first data point.

A complicated nineteenth century argument about agricultural and industrial commodity prices, of uncertain authorship, extended by a hardware merchant, has been compressed into seven words: a farmer predicted 2008.

The compression is the product. Every step that made the story shareable also made it less true. If the artifact cannot survive a provenance check, it is unlikely to survive a capital allocation decision.

Prediction by proximity

Grant the chart its best case anyway. Assume Benner drew every line himself.

The apparent accuracy is manufactured by proximity and by elastic categories.

“Panic” can absorb a recession, a correction, an inflation, a geopolitical rupture, or an event in an adjacent year. “Good times” can mean growth, high prices, or merely a moment that later looks like a decent exit. “Hard times” can mean a bear market, weak sentiment, or any period in which something eventually turned out to be cheap. Define the target broadly enough and widen the window enough, and history will always hand you a match.

But close is not a neutral word when you are moving money.

An investor who sold in 1927 did not simply dodge October 1929. He also handed back two years of one of the great bull markets in history, and he had to survive professionally while doing it. Someone who braced for the 2019 panic year and positioned defensively gave up a strong year in equities, and then the event that arrived had nothing to do with a nineteenth century commodity cycle. It was a virus.

Being early is indistinguishable from being wrong for anyone who has to report to a board, an investment committee, or a margin clerk.

And notice what happens to the misses. They vanish. The hits get screenshotted. This is survivorship bias applied not to funds but to ideas: a century and a half of charts, waves, cycles and warnings have been produced, nearly all of them forgotten, and the handful that can be retrofitted to later events keep getting rediscovered. The survival of a forecast is then mistaken for evidence of its accuracy.

Cycles are real. Clocks are not.

None of this requires denying that cycles exist. They plainly do, and anyone who has run a physical business has lived inside one.

Credit loosens. Leverage builds. Capacity gets added because returns look attractive and everyone is looking at the same returns. Supply overshoots. Prices break. Weak balance sheets fail, assets change hands cheaply, and the cycle reloads. Anybody who has watched a refining margin cycle, or a shale capex cycle, or a tanker rate cycle, knows the shape by feel.

Recurrence is real. Periodicity is fiction.

A capital cycle is not a planetary orbit. It runs on human decisions, and humans learn, institutions change, technologies emerge, central banks intervene, and, decisively, the act of anticipating the pattern changes the pattern. Markets are reflexive. They respond not to events but to beliefs about events, then to the strategies built on those beliefs, then to the consequences of thousands of participants adopting the same strategy at the same time.

October 1987 is the cleanest illustration. Portfolio insurance was designed to protect institutions by selling into declines. It was sound enough for one investor. Deployed simultaneously across the market, the selling triggered declines, which triggered more selling. The model did not merely observe the risk. At scale, it manufactured it.

Hold that thought. We are going to need it again shortly.

How capital actually dies

Long Term Capital Management is the case everyone reaches for, and usually for the wrong reason.

LTCM was not following anything as crude as a sepia chart. It was arguably the finest concentration of financial intellect ever assembled in one firm, including two Nobel laureates, trading small and genuinely observed pricing relationships among similar securities. It returned roughly twenty percent, then forty three, then forty one, then seventeen.

Here is the detail that matters, and it is an operator’s detail, not a mathematician’s.

At the end of 1997, LTCM returned capital to its investors without reducing the size of its book. The positions stayed. The equity underneath them shrank. By year end the fund was carrying something on the order of thirty dollars of debt for every dollar of capital.

Nobody voted to increase risk. Risk increased anyway, as a mechanical consequence of a decision that looked like discipline. That is how capital dies. Not in a dramatic wrong call, but in a structural change that no one re-underwrote because the model still said the trades were sound.

When Russia defaulted in August 1998, the spreads that were supposed to converge diverged, in nearly every case at once. Liquidity vanished. Positions that appeared diversified turned out to be one position: a leveraged bet that normal relationships and normal liquidity would return on a schedule the fund’s balance sheet could survive. It could not. On the twenty third of September, fourteen firms put roughly three and a half billion dollars into the fund in exchange for ninety percent of it, in a recapitalization the Federal Reserve Bank of New York brokered without lending a public dollar.

The lesson is not that the models failed. Every model fails to represent reality in full. That is what a model is for.

The lesson is that model confidence, leverage, concentration and illiquidity were stacked on top of one another until a temporary analytical error became a terminal one.

Ten years later the same epistemic mistake showed up wearing better clothes. Mortgage securities were rated using models built on historical default behavior from a period in which national home prices had not fallen, with assumptions about correlation across regional housing markets that turned out to be badly wrong. When prices fell everywhere at once, instruments assumed to be diversified failed together.

The Financial Crisis Inquiry Commission put it more plainly than any of us could. Its conclusion was that financial institutions and the rating agencies had come to treat mathematical models as reliable predictors of risk, and that in doing so they let the models stand in for judgment.

They let the models stand in for judgment. That is the whole essay in a line.

The regulators have not forgotten. In April of this year the Federal Reserve, the OCC and the FDIC rescinded the model risk framework that had governed banks since 2011 and replaced it with revised interagency guidance, on the view that models are simplifications whose usefulness and whose limitations arrive together, and that material model risk survives even rigorous validation.

That is not an argument against models. It is an argument against worshipping them.

The same error, in a nicer suit

Everything above happens in boardrooms too, and it is harder to see there because it is denominated in slides rather than basis points.

A single price deck carries a ten billion dollar project. Utilization is assumed to climb in a smooth line because it climbed in a smooth line before. Synergies are modeled as though identifying them in a spreadsheet makes them operationally inevitable. Demand is extrapolated from the most recent three years because that is the dataset most readily at hand. The base case hardens into the plan, the plan hardens into the budget, and by the time anyone asks what happens if the deck is wrong, the steel is on order.

The precision of the presentation conceals the fragility of the assumption. A strategy is not robust because the model balances.

And the failure is almost never the forecast. It is that no one wrote down which two or three variables the entire conclusion was resting on, and no one went back to look at them when the world moved. The forecast was wrong in the ordinary way all forecasts are wrong. The capital died because nobody had built anything that could survive being wrong.

The new pattern machine

Which brings us to the part of this I find genuinely worth worrying about.

The tempting move is to ask whether AI is the new railroad, the new dot com, the new tulip. It is the wrong question, and it is wrong in an instructive way, because it is a question about where we sit on a cycle. It assumes the schedule.

The better question is what happens when the tool we increasingly use to reason about the future is, by construction, a pattern extractor trained on the past.

A large model does not know that 2026 is not 2007. It knows what text about 2007 looked like. It is exceptionally good at producing the most probable continuation of a pattern, and it is exceptionally fluent while doing it, which means it delivers regression toward the historical consensus in the register of confident analysis. It is, in a precise sense, a machine for manufacturing the feeling the Benner chart manufactures. The pattern is found. The pattern is stated cleanly. The uncertainty is smoothed off, because uncertainty is not what fluent text sounds like.

Then recall 1987. The danger of portfolio insurance was not the logic. It was the correlation. Thousands of institutions running the same rule turned a hedge into an accelerant.

We are now installing broadly similar models, trained on broadly overlapping data, into the analytical layer of the same industries, at the same time, reaching similar conclusions from similar priors, and telling everyone the same thing at once. That is not a bubble question. That is a correlation question, and it is the one worth asking early.

The agencies are already asking it. Alongside the revised model risk guidance, the OCC, Federal Reserve and FDIC have said they intend to issue a request for information on model risk management that specifically addresses banks’ use of AI, including generative and agentic systems. That is the right question arriving at the right time, which is unusual enough to notice.

The correct posture is not to refuse the tools. The tools are extraordinary and I use them daily. The correct posture is to remember what they are: instruments that compress the past into a confident sentence. Confidence is the output. It is not the evidence.

The frictionless era

Meanwhile every remaining obstacle to acting on a hunch is being removed.

Prediction markets have industrialized. Total volume across CFTC registered prediction markets ran past twenty five billion dollars in 2025, and the number of listed event contracts went from roughly sixteen hundred a day in April 2025 to about a hundred and sixty two thousand a day a year later. That is a hundredfold increase in the supply of things to have an opinion about, and the CFTC is now building a framework to govern it.

Prediction markets are useful. They force beliefs to be quantified, they aggregate dispersed information, and they update. But a contract at seventy cents does not establish that an event is seventy percent likely. It establishes that capital is currently clearing at seventy cents, given the participants, liquidity, incentives and contract language in that market at that hour. That is information. It is not permission to stop thinking.

At the same time the friction on the retail side is gone. FINRA has eliminated the pattern day trader designation and the twenty five thousand dollar minimum equity requirement that stood since 2001, replacing them with real time intraday margin standards. The SEC approved it in April. It took effect the fourth of June, with firms phasing in through October of 2027, so your broker’s treatment may still vary.

Lower the barrier and you have not created an edge. You have only removed the thing that was slowing down the mistake.

The evidence on that is not close. Barber and Odean studied sixty six thousand four hundred sixty five households at a discount broker from 1991 to 1996. The most active traders earned 11.4 percent annually against a market returning 17.9. The average household turned over three quarters of its portfolio a year to underperform. Their explanation was overconfidence, and their title has aged better than anything else written on the subject: trading is hazardous to your wealth.

When every belief can instantly become a position, uncertainty starts to feel like a problem demanding action. A headline demands a trade. A chart demands an entry. A model output demands a decision. But activity is not analysis, and the ability to transact is not the presence of an opportunity.

The question is never whether the thing can be traded. It is whether you know why the person on the other side is willing to trade it with you.

What discipline actually looks like

The alternative to false certainty is not paralysis, and it is not the fashionable pose that nothing can be known. Businesses can be valued. Capital cycles can be read. Some outcomes are plainly more likely than others. The discipline is simply to keep three things separate that weak analysis always collapses into one.

A thesis explains why something creates value, and it names the causal mechanism. A forecast estimates how that mechanism might unfold. A decision determines how much capital, time and reputation to commit given that the forecast may be wrong. Strong analysis holds all three apart. Weak analysis fuses them into a single confident story and calls the story conviction.

In practice that means a small number of questions asked before the money moves, and asked again after it has.

Which is observation and which is interpretation. Revenue grew is an observation. Revenue will keep growing because the company has reached escape velocity is an interpretation wearing the clothes of an observation.

What is the base rate. Before asking whether this acquisition will work, ask how acquisitions of this type have generally worked. The specific case has to earn its departure from the record.

Which two or three assumptions are carrying the entire conclusion. Almost every model is driven by a handful of variables, and finding them is worth more than another decimal place on the output.

What would prove me wrong, and what would I do about it. If every decline is a buying opportunity and every delay is temporary and every contradictory fact is the market failing to understand, the thesis has stopped being a thesis and become an identity.

What happens if I am directionally right and temporally wrong. This is the one that kills people. LTCM’s trades eventually converged. The fund was not there to see it. Liquidity and timing are not secondary details. They determine whether you are still in the room when you turn out to have been correct.

Good leaders are not the ones with the best forecasts. They are the ones who know which assumptions matter, who size their bets accordingly, who protect the downside, who stage commitments where they can, who preserve the option to be wrong, and who update faster than their competitors.

Their advantage is not clairvoyance. It is preparedness.

The Point Taken

The Benner chart is not worthless. Its value is simply not the value assigned to it.

It is evidence that the hunger for a schedule is very old. It shows that investors have always converted recurring human behavior into claims of fixed numerical law, and that the conversion has always felt like insight rather than like appetite. That it still circulates, and still persuades serious people who allocate real money, tells us how little the hunger has changed in a hundred and fifty years.

We still want the card. We still want someone to tell us when to buy, when to sell, and when the panic arrives. We still prefer a clean line to an untidy distribution. And we will take that line from a nineteenth century hardware catalogue, a prediction market price, an analyst target, or a language model, because what we are actually purchasing is not information. It is relief.

The relief is the product being sold. The capital is what pays for it.

Use patterns as questions. Use probabilities as estimates. Use models as tools, and know precisely where each one stops describing the world.

Then build something that does not require prophecy to survive.

The future does not belong to those who predict it most confidently. It belongs to those who allocate capital, attention and effort most intelligently while knowing they may still be wrong.

© 2026 23.5 Strategies; The Point Taken™