Sustainable Aviation Fuel: A Hedge, Not a Hero

The fuel aviation bet its future on could cover seven and a half days of a single oil shock. The shortfall was never in the refinery capability. It was in the physics of feedstocks.

The fuel aviation bet its future on could cover seven and a half days of a single oil shock. The shortfall was never in the refinery capability. It was in the physics of feedstocks.

By Bryan J. Kaus

“You only find out who is swimming naked when the tide goes out.” - Warren Buffett

The Strait of Hormuz went quiet in the last days of February. The first two months of the year had been ordinary in fuel markets, prices sitting in the low-to-mid two-dollar-a-gallon range for weeks. Then the war started, the tankers stopped, and within weeks jet fuel in the United States ran from roughly two and a half dollars a gallon to nearly five. Carriers cut marginal flying, redeployed aircraft to higher-yield routes, and paid whatever the next cargo cost. They also reached, by reflex, for the fuel they had spent a decade calling the future of flying.

It was not there.

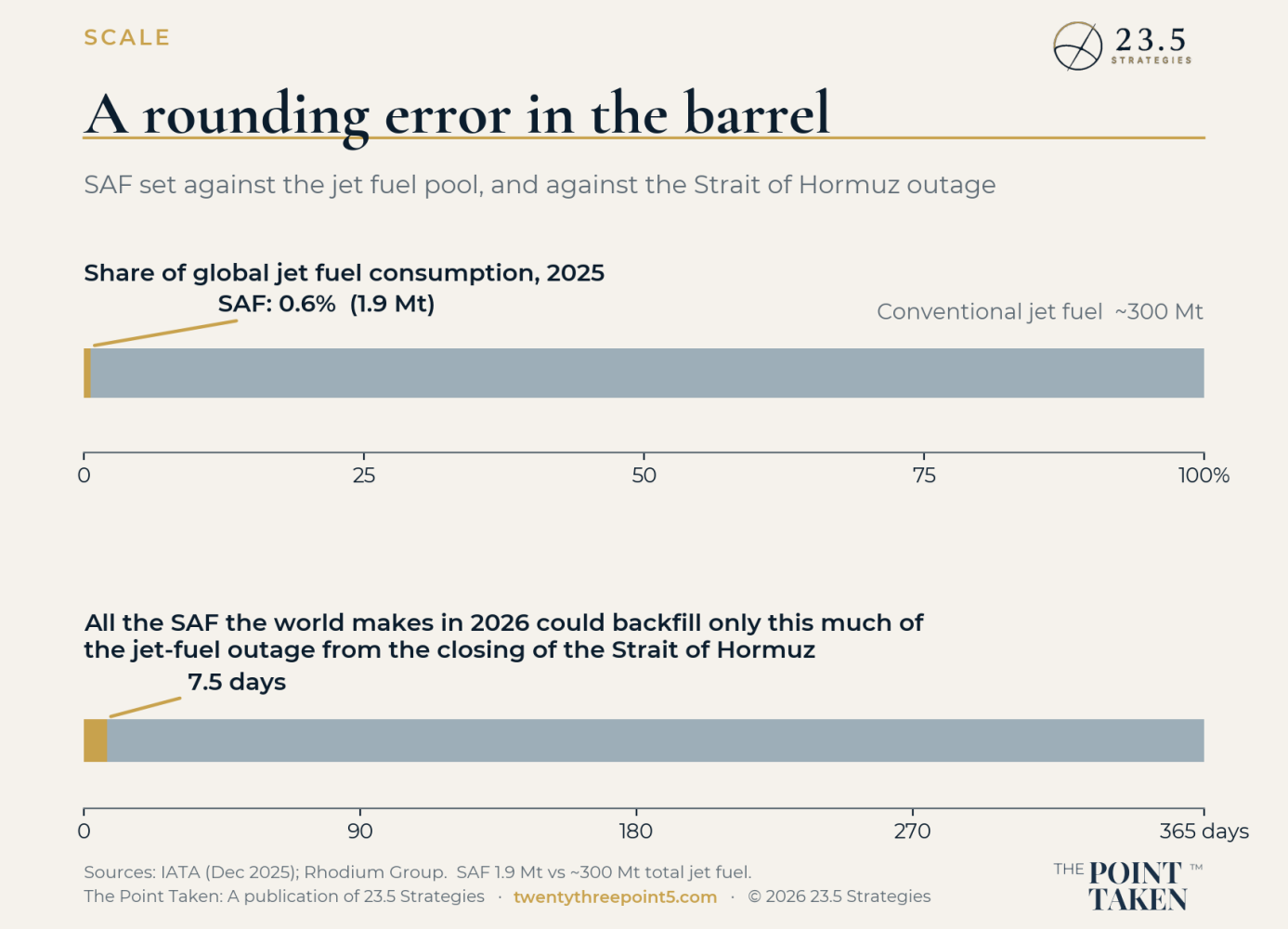

Add up all the sustainable aviation fuel the world will make this year and you have enough to replace about seven and a half days of what the Strait took off the market. Not seven and a half days of global jet demand. Seven and a half days of the disruption alone. The hedge that was supposed to matter most in a supply shock turned out to be a rounding error in the one that came.

The gap the crunch exposed

The Wall Street Journal said it plainly in early June. Airlines had called sustainable fuel the future, and when the crisis arrived there was almost none of it to reach for. The arithmetic is not subtle. SAF made up about six-tenths of one percent of jet fuel last year. Total jet consumption runs near three hundred million tonnes a year. SAF output sits around two million tonnes. Four years ago the international aviation body expected this year’s volumes near five million tonnes. We are at less than half of that, and growth is slowing, not accelerating.

The head of the airline trade group called the progress disappointing and pointed at fuel producers and at policy. Both deserve a share of the blame. Neither is the constraint that actually binds. A decade of mandates in Europe and the UK, billions in premiums paid by airlines for the little SAF that exists, and the product still has not reached commercial scale anywhere on earth. When effort that large produces a result that small, the problem is not effort or ambition. It is physics and geography.

It was never the refinery

Here is what the run of disappointing numbers tends to obscure. The technology works.

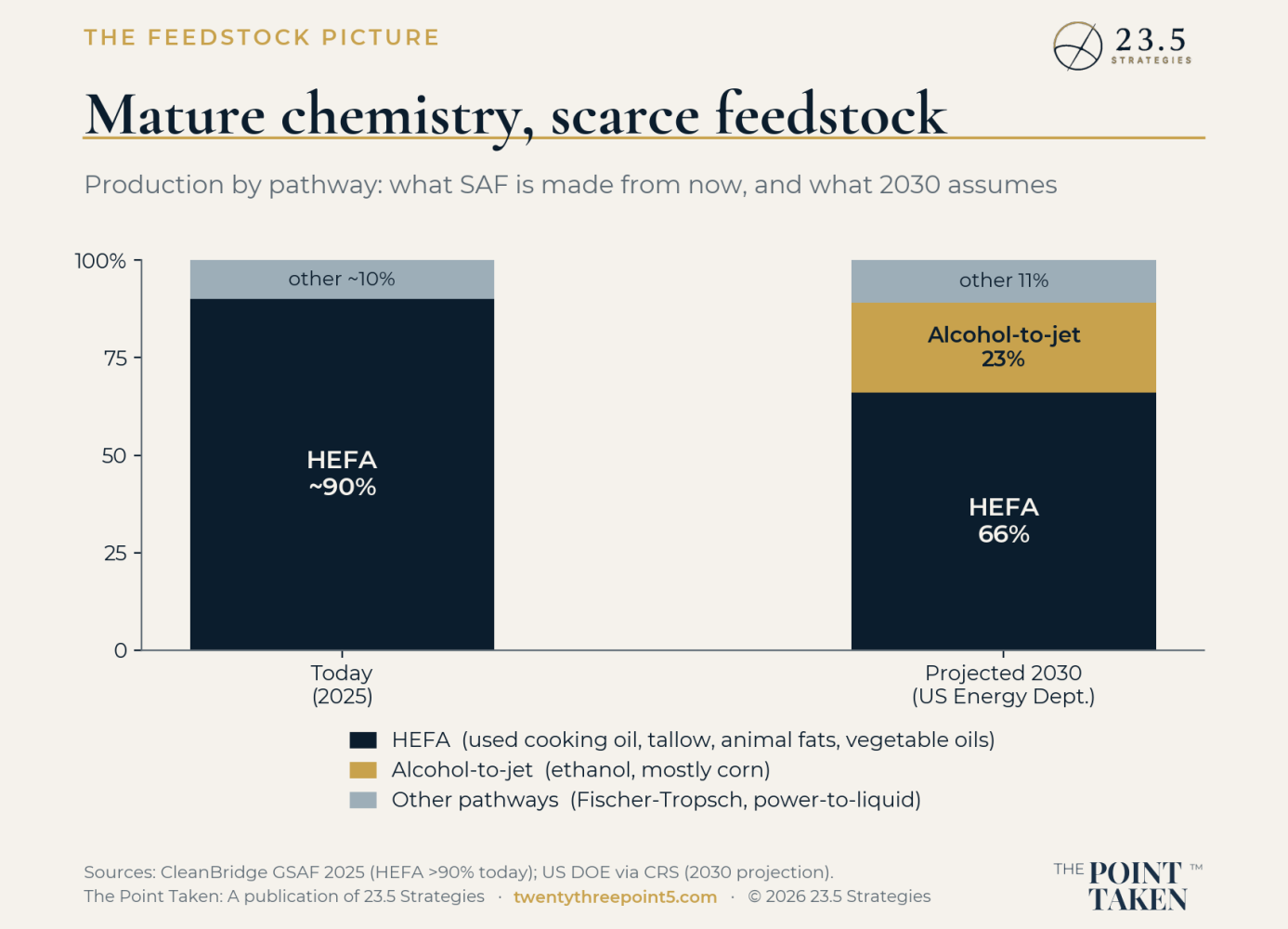

The dominant production route, hydroprocessed esters and fatty acids, is mature and commercial. It accounts for roughly nine in ten gallons of SAF made today. The fuel is a true drop-in. It burns like Jet A, moves through the same pipelines, fuels the same engines, needs no new aircraft and no new airport plumbing. The plants exist. Many are converted renewable diesel units that already know how to run the process. If the molecule works and the units run, the obvious question is why there is so little of it.

Because the process eats lipids. Used cooking oil, tallow, animal fats, vegetable oils. And there is not enough of that to matter at the scale aviation burns fuel. The refinery was never the bottleneck. The grease was.

The tell was the fraud

When a market starts counterfeiting its own raw material, that tells you exactly where the scarcity sits.

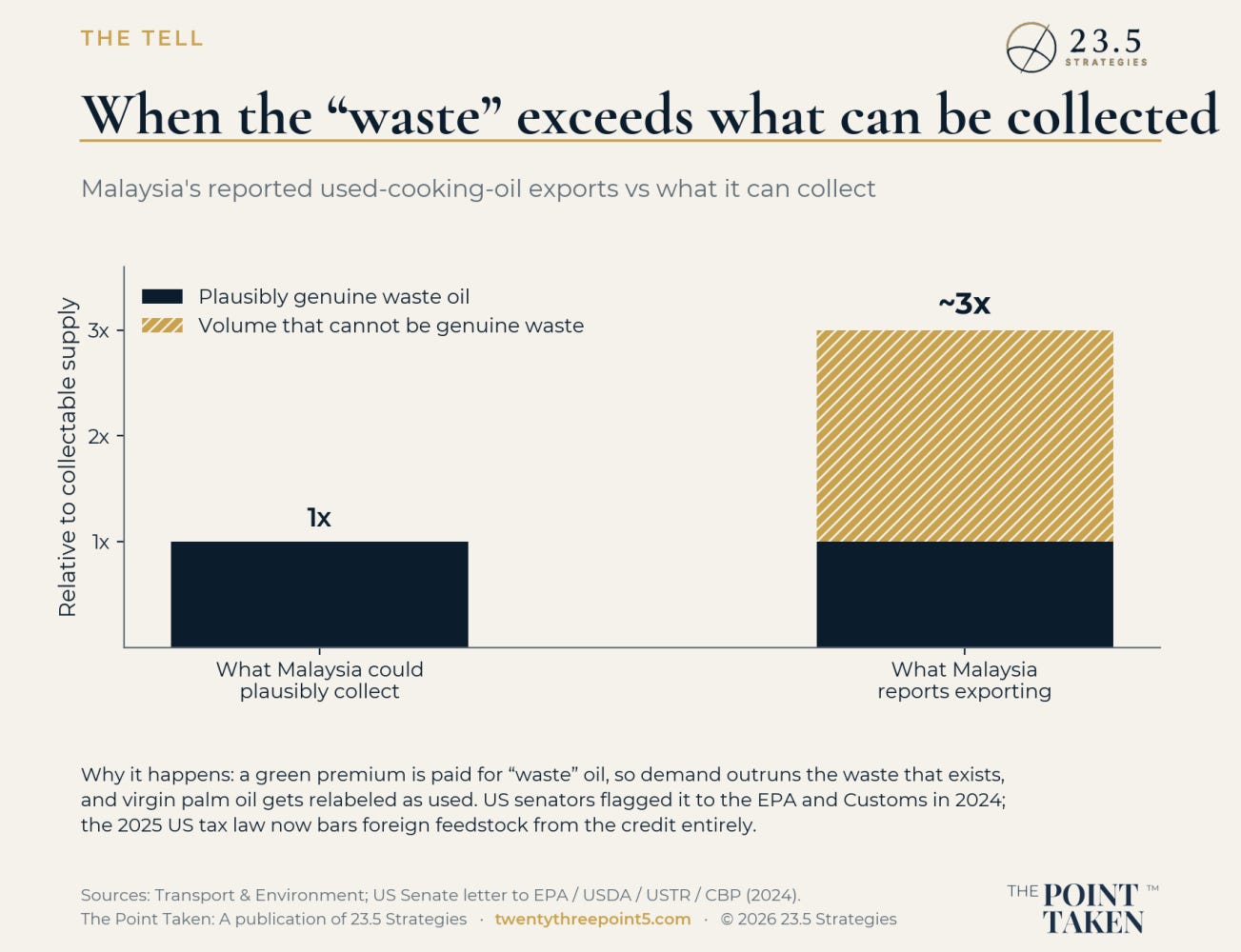

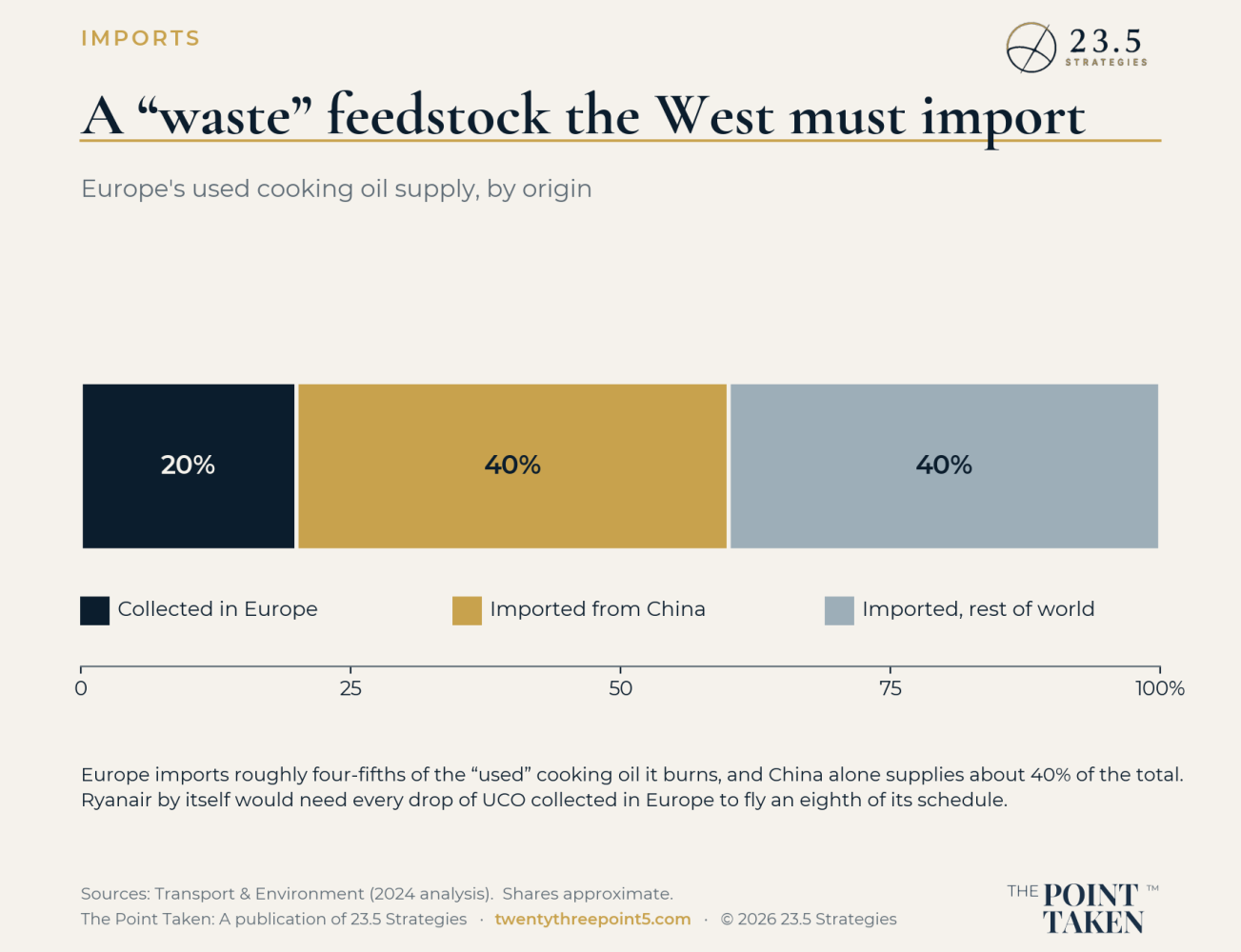

Europe now imports something like four-fifths of the “used” cooking oil it consumes. China supplies close to forty percent of that. Malaysia exports roughly three times more used cooking oil than the country could plausibly collect, which is not a logistics miracle. It is virgin palm oil wearing a waste label to capture the green premium. The pattern got serious enough that a bipartisan group of farm-state senators wrote to the EPA, Customs, and the trade representative asking for enforcement. The United States, a country of restaurants and fryers, now imports a waste commodity it produces in abundance, because demand for the molecule has outrun the molecule.

Run the volumes and the ceiling is obvious. Ryanair alone would need every drop of used cooking oil collected in Europe to fly an eighth of its schedule. Global targets for 2030 would require at least twice the used cooking oil that the United States, Europe, and China can collect combined. You can legislate a blending mandate. You cannot legislate grease into existence.

Which means it is agriculture and logistics

Reframe the whole problem and it stops looking like a fuel question.

SAF at scale is a collection problem. The feedstock molecules are real and they exist, but they sit dispersed across millions of fields, fryers, and rendering lines, and somebody has to aggregate them, verify them, and haul them to a converter. That is supply chain work. It is trucks, rail, storage, chain-of-custody documents, and the unglamorous discipline of knowing that the thing in the tank is the thing on the certificate. The pathways that scale are the ones that plug into a collection and logistics network that already exists, not the ones that require building that network from nothing.

Some of the answer is agronomic. Cover crops like winter camelina and carinata can be layered into existing rotations and fallow ground, adding oilseed feedstock and farmer revenue without displacing food acres. That is promising and slow. The machine that already exists, fully built and fully paid for, is corn.

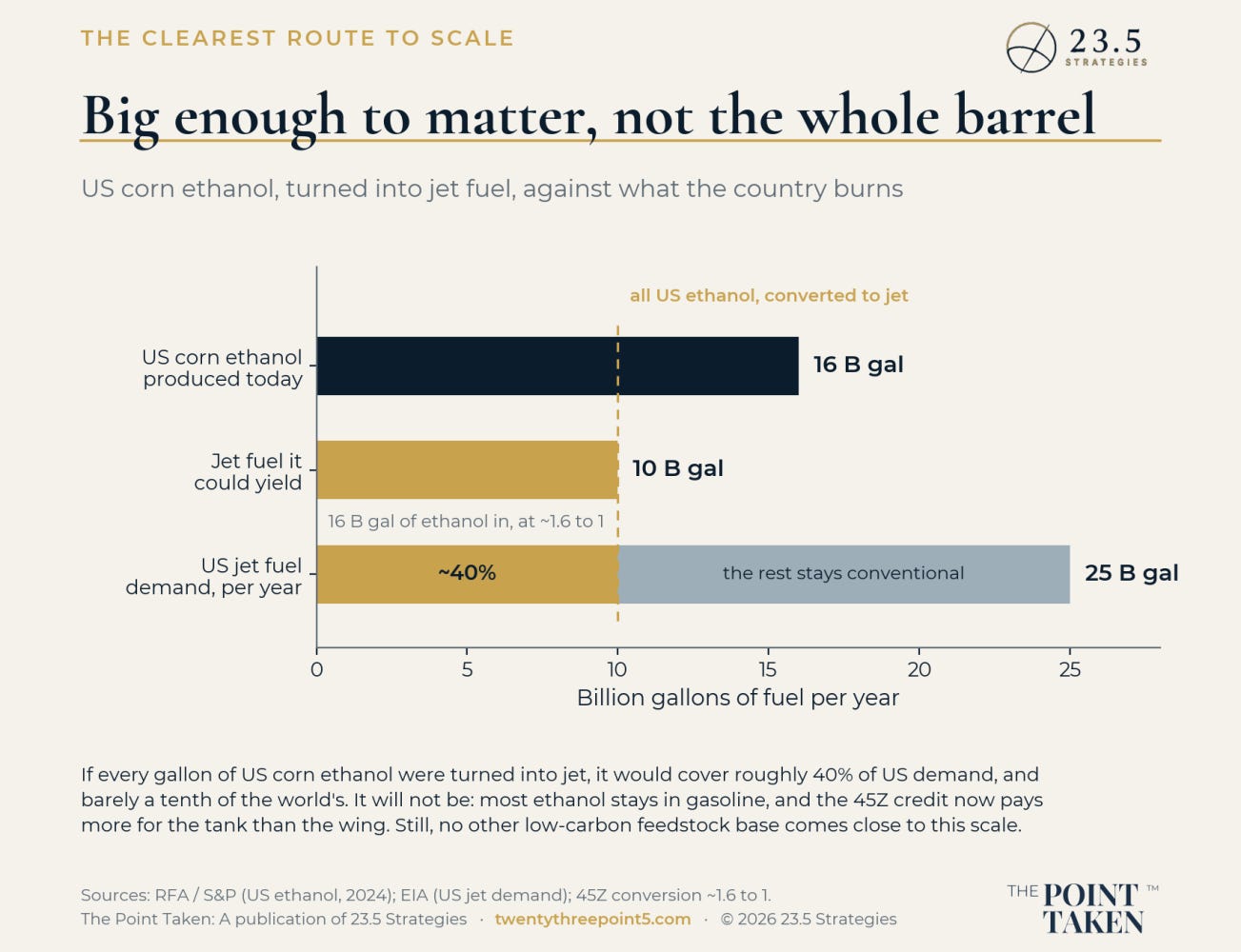

The clearest route to scale

The pathway with the cleanest line to volume is alcohol-to-jet, and in the United States that means ethanol.

The country already makes on the order of sixteen billion gallons of ethanol a year, almost all of it from corn, sitting on top of an agricultural and rail logistics system that took a century to build and is already amortized. The feedstock aggregation problem that strangles the grease pathways is, for corn, already solved. That capacity could in principle yield roughly ten billion gallons of renewable jet, close to forty percent of the twenty-five billion the country burns in a year. The plants are starting to come. Gevo’s Net-Zero One in Lake Preston, LanzaJet’s Freedom Pines in Georgia, Summit’s next-generation projects. Industry’s own assessment is that ethanol-to-jet is one of the few routes that can plausibly reach real commercial scale. The capital-heavy routes, Fischer-Tropsch gasification and power-to-liquid e-fuels, are real and probably necessary by mid-century, but they are next-decade stories that require building both the conversion plants and the feedstock systems at once. The grease route hits its ceiling around 2030 no matter how many units get built.

And every pathway here still assumes the fuel has to pour into the engines already flying. Change the engine and you change the question. Hydrogen, batteries on the short hops, airframes built to burn less, those are real and worth chasing. But they replace the fleet rather than fuel it, which makes them a mid-century project, not a this-decade one. For the aircraft already in the sky, the choice is drop-in liquid or nothing, and drop-in liquid is bounded by what the land can grow and the waste stream can yield.

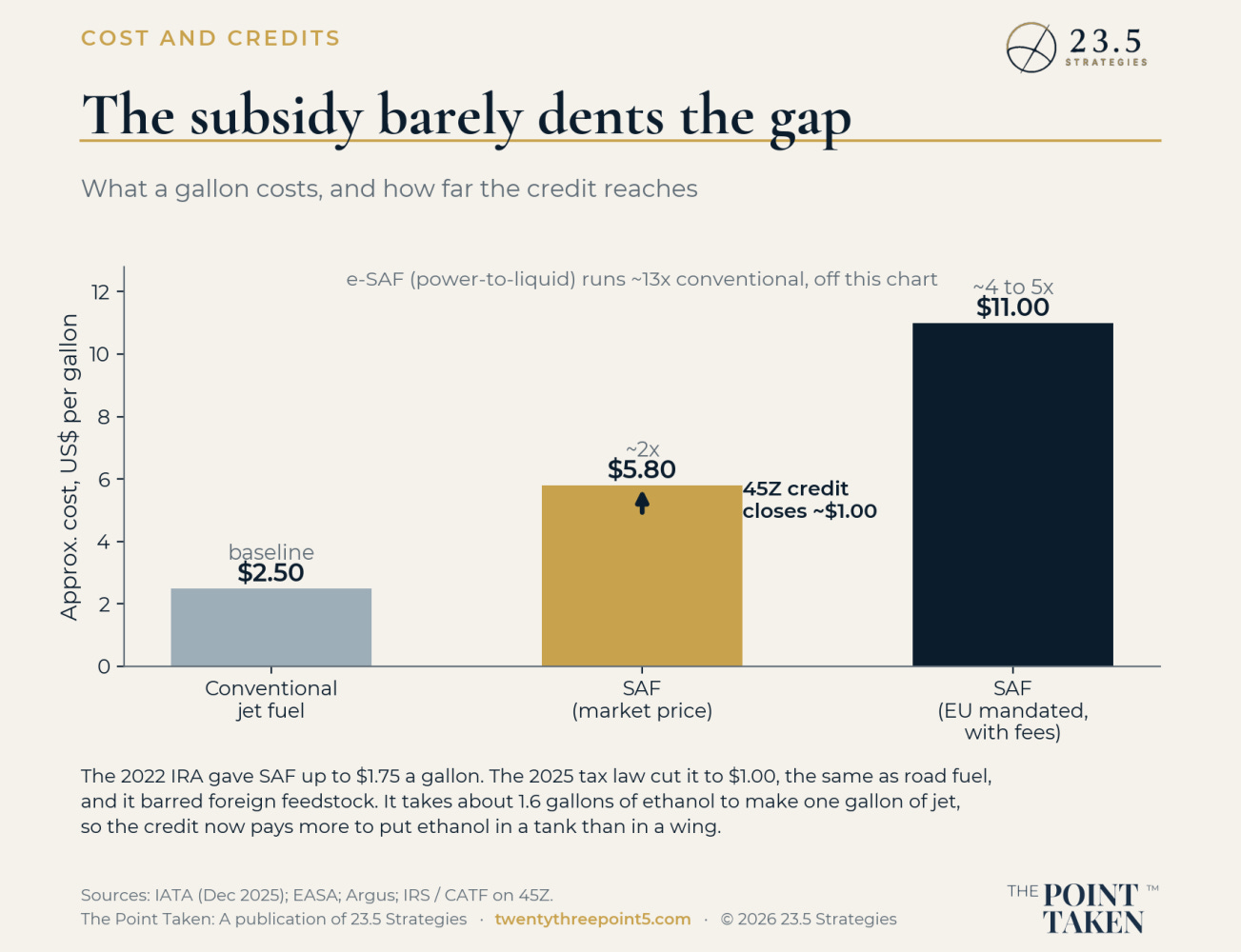

Now the catch, and this is where the original framing needs sharpening. The constraint on the most scalable pathway is, at this moment, policy. Sustainable fuel runs about twice conventional jet at the market and four to five times where mandates force it, so the economics never close on their own, and a production credit was meant to bridge the difference. Instead it pays more to put a gallon of ethanol into a gas tank than into a wing, and it takes about one and six-tenths gallons of ethanol to make a gallon of jet. The tax bill passed last July cut the SAF credit from a dollar seventy-five to a dollar even while preserving the road-fuel value. So the single pathway with built-in logistics scale is the one current incentives quietly underpay.

That is the honest answer to whether this was a policy problem or a feedstock problem. It was both, in a specific order. Policy decides which feedstock gets chased. Feedstock decides whether the chase ever reaches scale. The mandates summoned a decade of demand for waste oils. They could not summon the oils. The binding constraint, the one that does not bend to a signature, is the physical, agricultural, logistical one underneath.

The diesel echo

There is a second-order loop worth holding in view. The same disruption that broke the jet market is hitting diesel, because refiners prioritize diesel over jet when they allocate constrained barrels. American farmers are absorbing the worst diesel shock since 2022 right now. And the most scalable SAF feedstock is grown, harvested, and hauled with that diesel. The resilient fuel of the future runs, today, through an agricultural system that is exposed to the very shock it is meant to hedge. Resilience that runs through the field runs through the diesel pump too. Real damage from a supply shock tends to arrive on a lag, downstream, after the headline price has already moved on.

The Point Taken

For a decade the industry treated sustainable aviation fuel as a problem of chemistry and subsidy. The crunch after Hormuz revealed it as a problem of collection and logistics wearing a chemistry costume. The pathway with the clearest route to commercial scale is not the most elegant molecule or the cleverest process. It is the one already sitting on an agricultural supply chain that exists, paid for, and running.

That pathway can make SAF a viable product. Where the feedstock economics already work, low-carbon ethanol in the corn belt, waste oil with provenance you can actually verify, SAF earns a durable place in the blend and stands on commercial logic rather than mandate. Everywhere it leans on imported grease or fuel that still has to be invented, it stays boutique and subsidy-fed. The work was never inventing the fuel. The work is assembling the feedstock honestly, at volume, and pointing the incentives so the gallon flows to the aircraft instead of the automobile.

None of that makes the fuel a failure. It makes it a hedge, which is a more honest thing to be than a replacement. The blend that exists today is too small to save an airline in the week a strait closes, and no credit conjures more of it overnight. But a barrel that draws on more than one source is a sturdier barrel over the years it takes to build that source, and a hedge like that is worth paying for on its own terms. The case for sustainable fuel was always a case for optionality. It was never a case for substitution.

The future of flight was never going to be refined into being. It was going to be grown, collected, and hauled. We just kept studying the wrong end of the supply chain.